Mutual Funds

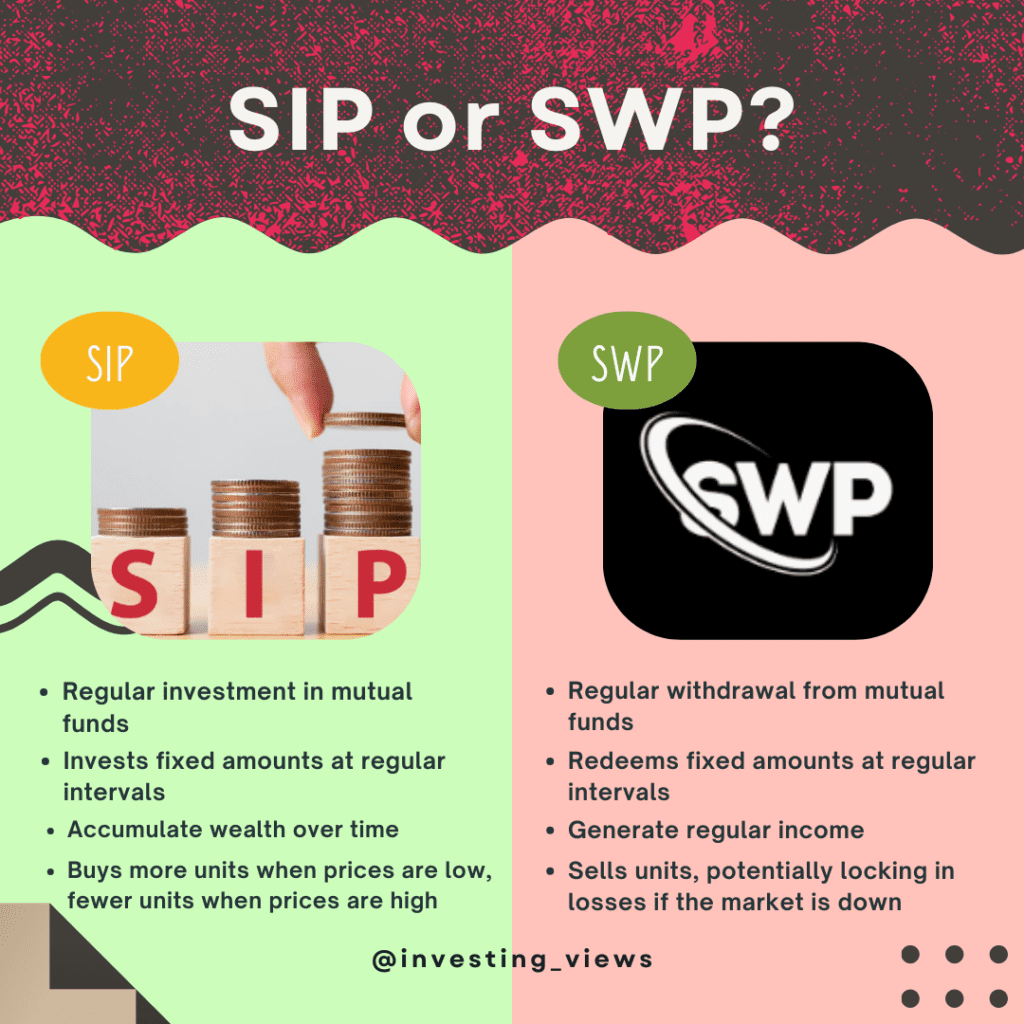

SIP VS SWP

When it comes to investing in mutual funds, two popular strategies often come to mind:

Systematic Investment Plan and Systematic Withdrawal Plan( SIP VS SWP ).

Both serve different financial purposes and can be valuable depending on your goals. In this blog, we’ll explore what SIP and SWP are, and how they work, and we’ll also look at potential returns over 10 to 20 years to help you understand which one might be the best choice for you.

What is SIP (Systematic Investment Plan)?

SIP stands for Systematic Investment Plan, where you invest a fixed amount of money at regular intervals, usually monthly, into a mutual fund. One of the key benefits of SIP is its simplicity—you can start with a small amount and gradually build your investment over time. By investing regularly, you can take advantage of market fluctuations, buying more units when prices are low and fewer when prices are high. Over the long term, this can result in a better average purchase price and potentially higher returns.

Example SIP Calculation:

Let’s say you decide to invest ₹10,000 per month in a mutual fund through SIP. Assuming an average annual return of 12%, here’s how much you could accumulate over time:

- After 10 Years:

- Total Investment: ₹10,000 * 12 * 10 = ₹12,00,000

- Estimated Return: ₹23,00,000

- Total Value: ₹12,00,000 + ₹23,00,000 = ₹35,00,000

- After 20 Years:

- Total Investment: ₹10,000 * 12 * 20 = ₹24,00,000

- Estimated Return: ₹78,00,000

- Total Value: ₹24,00,000 + ₹78,00,000 = ₹1,02,00,000

These calculations show that with regular investing, your money can grow significantly over time, making SIP a powerful tool for long-term wealth building.

Calculate your own goal using the SIP Calculator:- SIP Calculator

Who Should Choose SIP?

SIP is ideal for everyone, especially those who want to build wealth gradually and have a regular source of income. It’s particularly suitable for long-term goals such as buying a home, funding education or saving for retirement. SIPs help in instilling a disciplined savings habit, making them a great option for those new to investing.

What is SWP (Systematic Withdrawal Plan)?

SWP stands for Systematic Withdrawal Plan. Unlike SIP, where you invest regularly, SWP allows you to withdraw a fixed amount of money from your mutual fund investment at regular intervals, typically monthly. This method is especially useful for those who need a steady income, such as retirees. With SWP, you withdraw only a portion of your investment, allowing the rest of your money to continue growing.

Example SWP Calculation:

Let’s assume you have accumulated ₹20,00,000 in a mutual fund and you wish to withdraw ₹10,000 per month. If your investment continues to grow at an average rate of 12% annually, here’s how it could play out:

- After 10 Years:

- Total Withdrawal: ₹10,000 * 12 * 10 = ₹12,00,000

- Remaining Investment Value: ₹26,00,000 (even after withdrawals, thanks to growth)

- After 20 Years:

- Total Withdrawal: ₹10,000 * 12 * 20 = ₹24,00,000

- Remaining Investment Value: ₹48,00,000

This shows that even while withdrawing regularly, your investment can continue to grow, providing you with a stable income while preserving your capital.

Also read : Stocks to Watch : Key Listings, TCS Results, and Intraday Opportunities

Who Should Choose SWP?

SWP is best for individuals who have already invested significantly and now need a regular income stream. It’s particularly beneficial for retirees who need consistent funds for living expenses. SWP allows you to manage your withdrawals systematically while still keeping a portion of your money invested.

Conclusion:

Both SIP and SWP have their own advantages and serve different financial purposes. If you’re looking to accumulate wealth over time, SIP is a solid choice. On the other hand, if you’ve already accumulated wealth and are looking for a steady income, SWP is the better option. The example calculations above show how each plan can grow your wealth or provide income, making it easier to decide which plan suits your needs.

Remember, whether you choose SIP or SWP, the key is to stay disciplined and review your investments regularly to ensure they align with your financial goals.

To Calculate your returns click here: SIP CALCULATOR